| 1. | |

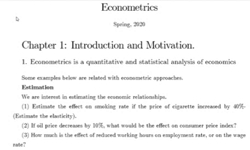

계량_1주(1) | Chapter 1 : Intraduction and Motivarion |  |

|

계량_1주(2) | Chapter 2 : Simple Linear regression Model /Many parts in this chapter are related with the last couple of chapters of ecomonics statistics | |

|

| 2. | |

계량_2주 | 전 차시 복습 | |

|

계량_2주(복사본) | 전 차시 복습 | |

|

| 3. | |

계량_3주(1) | 전 차시 복습, Chapter 3 : Interval Estimation and Hypothesis Thesting in a Linear Regressin Model (stat. review) | |

|

계량_3주(2) | 전 차시 복습, Chapter 4 : Goodness of fit(model specifications), and some modeling Issues | |

|

| 4. | |

계량_4주(1) | Chapter 4 : Goodness of fit(model specifications), and some modeling Issues | |

|

계량_4주(2) | 전 차시 복습, Chapter 5 : Multiple regressions | |

|

| 5. | |

계량_5주 | 전 차시 복습, Chapter 6 : Further Inference in Multiple Regression Model Hypothesis testing and Model specification | |

| 6. | |

계량_6주(1) | Chapter 6 : Further Inference in Multiple Regression Model | |

|

계량_6주(2) | Chapter 7 : Nonlinear relations /In this chapter, we introduce some nonlinear models. | |

|

| 7. | |

계량_7주(1) | 중간시험 공지, Chapter 8 : Heteroskedasticity(Unequal Variance) |

|

|

계량_7주(2) | Chapter 8 : Heteroskedasticity(Unequal Variance) | |

|

| 8. | |

계량_8주 | 중간시험 공지와 Review | |

| 9. | |

계량_9주 | Chapter 9 : Dynamic Models, Autocorrelation, and Forecasting /In this section, we consider correlations of errors between the two different time point, denoted as autocorrelation | |

| 10. | |

계량_10주(1) | 중간시험 채점기준, Chapter 9 : Dynamic Models, Autocorrelation, and Forecastin | |

|

계량_10주(2) | 전 차시 복습, Chapter 10: Introduction to Time series | |

|

| 11. | |

계량_11주(1) | Chapter 10: Introduction to Time series | |

|

계량_11주(2) | Chapter 10: Introduction to Time series | |

|

| 12. | |

계량_12주(1) | 전 차시 복습, Chapter 11: Endogeneity and Instrumental Variables Estimation | |

|

계량_12주(2) | Chapter 11: Endogeneity and Instrumental Variables Estimation | |

|

| 13. | |

계량_13주(1) | 전 차시 복습, Chapter 11: Endogeneity and Instrumental Variables Estimation Chapter 12 : Volatility ARCH(AutoRegressive Conditional Heteroskedasticity) Models | |

|

계량_13주(2) | Chapter 12 : Volatility ARCH(AutoRegressive Conditional Heteroskedasticity) Models | |

|

| 14. | |

계량_14주(1) | 전 차시 복습, Chapter 13 : Multiple time series and AR(Vector Autoregression)models /In this chapter, we study a model for multipe time series variable | |

|

계량_14주(2) | Chapter 13 : Multiple time series and AR(Vector | |

|

| 15. | |

계량_15주(1) | Chapter 14 : Regression with Panel data | |

|

계량_15주(2) | Chapter 14 : Regression with Panel data Chapter 15 : Models with discrete choice variables /we consider a model where dependent variable take discrete values. | |

|

|

계량_16주 | 기말 시험 범위 Review | |

대구광역시 동구 동내로 64(동내동 1119) 우)41061

대구광역시 동구 동내로 64(동내동 1119) 우)41061

COPYRIGHT keris. all rights reserved